UNFI Reports Solid Q2 Fiscal 2026 Earnings; Continues to Advance Value Creation Strategy

March 10, 2026 3 minute read

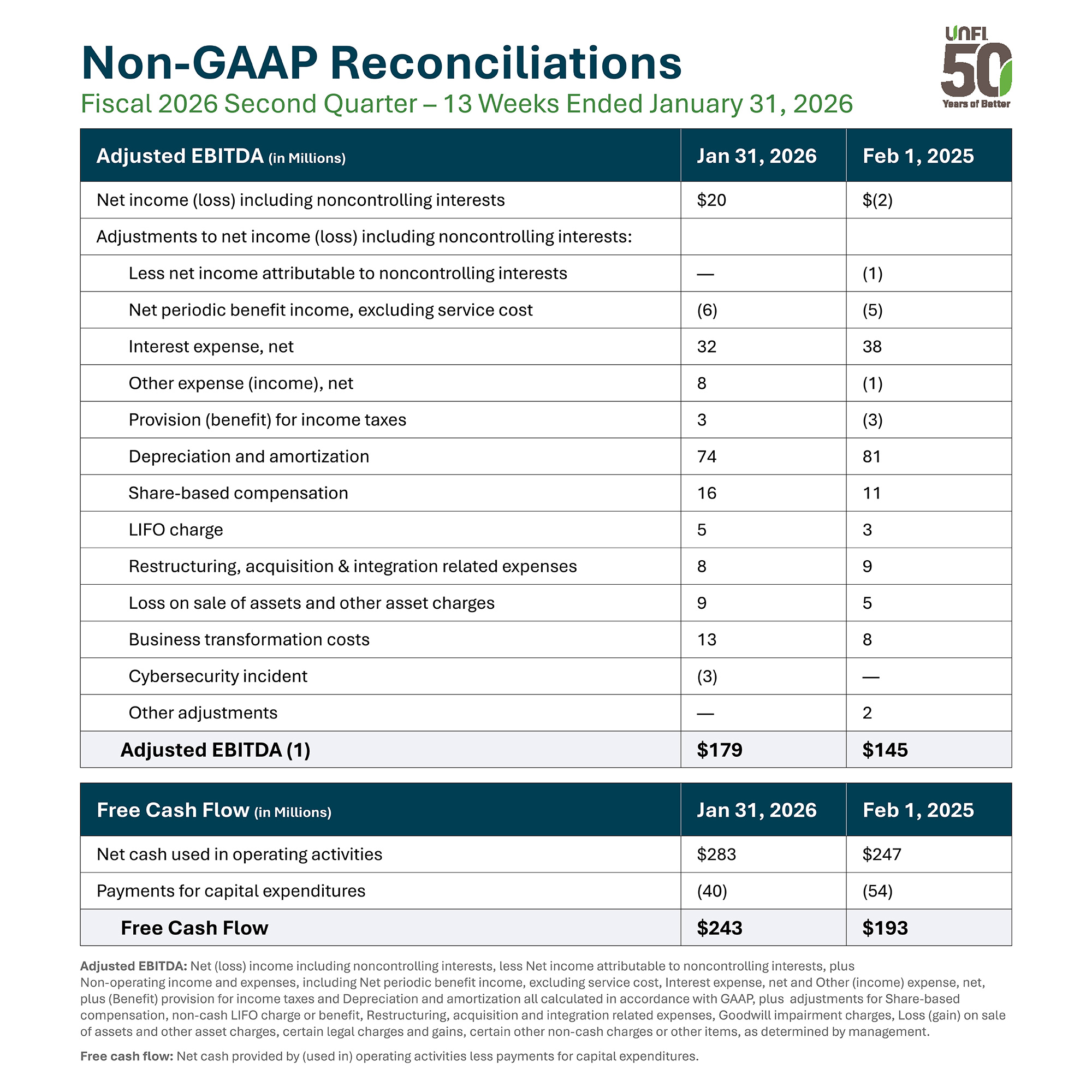

Today, UNFI reported second quarter fiscal 2026 results that reflect strong execution of the company’s value creation strategy. Profitability (measured by Adjusted EBITDA) increased 23.4% to $179 million, and the company generated $243 million in free cash flow - $50 million more than in last year’s second quarter. Both results exceeded projections, supported by strong, +7% growth in natural products and continued gains in effectiveness and efficiency.

While the large majority of UNFI’s customer base grew, total net sales of $7.9 billion represents a decline of 2.6%, primarily due to planned network optimization.

“In the second quarter, disciplined execution of our value creation strategy delivered growth in profitability and free cash flow ahead of our projections, which enabled us to further strengthen our balance sheet and increase our financial flexibility. With a sharpened focus on our growing $90 billion target addressable market, we are working to help differentiating retailers continue to accelerate profitable growth in a dynamic marketplace,” said Sandy Douglas, UNFI’s CEO.

Strengthening capabilities to add value for customers and suppliers

UNFI shared progress on the capability-build efforts highlighted at its 2025 Investor Day, including the expansion of its private label assortment with nearly 50 new, on trend product innovations that are seeing encouraging early adoption from retail partners.

The company also continued the rollout of an AI-powered supply chain planning platform, which together with improved processes is helping the company improve order fill rates and more efficiently manage product inventory.

Operational discipline delivering results

UNFI continued to advance its lean transformation, expanding lean daily management (LDM) to 36 distribution centers through the quarter’s end. The company also held a dozen process improvement workshops to enhance the seasonal item buying process, reduce new customer onboarding time, and improve out of stock product rates.

“Our second quarter results reflect the continued strengthening of lean practices across the organization, driving measurable gains in safety, quality, delivery and cost,” said Matteo Tarditi, President and Chief Financial Officer. “Since the prior year quarter, we have reduced shrink by over 11% while throughput and on-time deliveries have both increased nearly 7% each. We’re still in the early stages of our lean transformation and believe there is significant value to be unlocked for customers, suppliers, associates, and shareholders as we continue our lean journey in the months and years ahead.”

UNFI raised its full year outlook for both Adjusted EBITDA and Adjusted EPS and now expects approximately $330 million of free cash flow for fiscal 2026. The company lowered full-year sales expectations from $31 to $31.4 billion, a nearly 1.9% change at the midpoint, due to optimization work that is ahead of schedule, as well as some deceleration in food retail sales in a dynamic macroeconomic environment.

UNFI expects that its strong new business pipeline, combined with the cycling of larger optimization actions in Q1 fiscal 2027, will allow the company’s sales to return to low single digit growth in fiscal 2027.

“Looking ahead, our new business pipeline is strong. And we remain committed to continuously improving our effectiveness and efficiency, delivering our updated outlook, and strengthening our capabilities to create long-term value for our customers, suppliers, associates, and shareholders,” said Sandy Douglas, CEO

For more details, read UNFI’s press release, or listen to the recording of its public earnings call.

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995: Statements in this press release regarding the Company’s business that are not historical facts are “forward-looking statements” that involve risks and uncertainties and are based on current expectations and management estimates; actual results may differ materially. The risks and uncertainties which could impact these statements are described in the Company’s filings under the Securities Exchange Act of 1934, as amended, including under the section entitled “Risk Factors” in the Company’s annual report on Form 10-K for the year ended August 3, 2024 filed with the Securities and Exchange Commission (the “SEC”) on October 1, 2024 and other filings the Company makes with the SEC, and include, but are not limited to, our dependence on principal customers; the relatively low margins of our business, which are sensitive to inflationary and deflationary pressures and intense competition, including as a result of the continuing consolidation of retailers and the growth of consumer choices for grocery and consumable purchases; our ability to realize the anticipated benefits of our strategic initiatives; changes in relationships with our suppliers; our ability to develop, implement, operate and maintain, and rely on third parties to operate and maintain, reliable and secure technology systems, and the effectiveness of the Company’s business continuity plans in response to an incident impacting the Company’s technology systems, such as the unauthorized incident on its technology systems; labor and other workforce shortages and challenges; the addition or loss of significant customers or material changes to our relationships with these customers; our ability to realize anticipated benefits of strategic transactions; our ability to continue to grow sales, including of our higher margin natural and organic foods and non-food products; our ability to maintain sufficient volume in our Natural and Conventional businesses to support our operating infrastructure; our ability to access additional capital; increases in healthcare, pension and other costs under our single employer benefit plan and multiemployer benefit plans; the potential for additional asset impairment charges; our sensitivity to general economic conditions including inflation, tariff policy and changes in disposable income levels and consumer purchasing habits; our ability to timely and successfully deploy our warehouse management system throughout our distribution centers and our transportation management system across the Company and to achieve efficiencies and cost savings from these efforts; the potential for disruptions in our supply chain or our distribution capabilities from circumstances beyond our control, including due to lack of long-term contracts, severe weather, labor shortages or work stoppages or otherwise; the effect of adverse decisions in, or settlement of, litigation or other proceedings to which we are subject; moderated supplier promotional activity, including decreased forward buying opportunities; union-organizing activities that could cause labor relations difficulties and increased costs; changes in tax laws and regulations, and actions by federal, state and local taxing authorities related to the interpretation and application of such tax laws and regulations; our ability to maintain food quality and safety; and volatility in fuel costs. Any forward-looking statements are made pursuant to the Private Securities Litigation Reform Act of 1995 and, as such, speak only as of the date made. The Company is not undertaking to update any information in the foregoing reports until the effective date of its future reports required by applicable laws. Any estimates of future results of operations are based on a number of assumptions, many of which are outside the Company’s control and should not be construed in any manner as a guarantee that such results will in fact occur. These estimates are subject to change and could differ materially from final reported results. The Company may from time to time update these publicly announced estimates, but it is not obligated to do so.

Non-GAAP Financial Measures: To supplement the financial information presented on a U.S. generally accepted accounting principles (“GAAP”) basis, the Company has included in this press release the non-GAAP financial measures Adjusted EBITDA, Adjusted EPS, adjusted effective tax rate, free cash flow, net debt to Adjusted EBITDA leverage ratio and Capital and cloud implementation expenditures. Adjusted EBITDA is a consolidated measure which the Company reconciles by adding Net (loss) income including noncontrolling interests, less Net income attributable to noncontrolling interests, plus Non-operating income and expenses, including Net periodic benefit income, excluding service cost, Interest expense, net and Other (income) expense, net, plus (Benefit) provision for income taxes and Depreciation and amortization all calculated in accordance with GAAP, plus adjustments for Share-based compensation, non-cash LIFO charge or benefit, Restructuring, acquisition and integration related expenses, Goodwill impairment charges, Loss (gain) on sale of assets and other asset charges, certain legal charges and gains, and certain other non-cash charges or other items, as determined by management. Adjusted EPS is a consolidated measure, which the Company reconciles by adding Net (loss) income attributable to UNFI plus the LIFO charge or benefit, Goodwill impairment benefits and charges, Restructuring, acquisition, and integration related expenses, gains and losses on sales of assets, certain legal charges and gains, surplus property depreciation and interest expense, losses on debt extinguishment, the impact of diluted shares when GAAP earnings is presented as a loss and non-GAAP earnings represent income, and the tax impact of adjustments and the adjusted effective tax rate, which tax impact is calculated using the adjusted effective tax rate, and certain other non-cash charges or items, as determined by management. The adjusted effective tax rate is calculated based on adjusted net income before tax and excludes the potential impact of changes to uncertain tax positions, valuation allowances, tax impacts related to the vesting of share-based compensation awards and discrete GAAP tax items which could impact the comparability of the operational effective tax rate. Free cash flow is defined as net cash provided by operating activities less payments for capital expenditures. Net debt to Adjusted EBITDA leverage ratio is defined as the total carrying value of the Company’s outstanding short- and long-term debt and finance lease liabilities less net cash and cash equivalents, the sum of which is divided by the trailing four quarters Adjusted EBITDA. Capital and cloud implementation expenditures is defined as the sum of payments for capital expenditures and cloud technology implementation expenditures.